Key Takeaways

- A large refund is an interest-free loan to the government, while a big bill suggests you are at risk for IRS underpayment penalties.

- Updating your Form W-4 by late April allows you to spread adjustments across the majority of the year, minimizing the impact on your monthly budget.

- For standard situations, use the IRS Tax Withholding Estimator to calculate your withholding.

- For complex scenarios (like RSUs, side hustles, or reaching credit caps), use manual calculation to ensure precision.

- If you received a large refund, you can increase your deductions in Step 4(b) or claim more credits in Step 3 of your W-4.

- If you had a big tax bill, enter the exact dollar amount you want withheld extra per pay period in Step 4(c).

Were you shocked by a massive tax bill or surprised by a huge refund?

Either way, that probably means your ‘set it and forget it’ withholding strategy has lost touch with your actual income.

Let’s get your withholding right while we still have time to spread the adjustment across the majority of the year, so your monthly budget stays manageable.

When should I adjust my withholding?

It’s important to revisit your Form W-4 after filing your tax return. Because your recent tax results are like a financial physical, highlighting exactly where your withholding stands relative to your actual liability.

Specifically, we should evaluate your withholding if…

1. You had a large tax bill this tax season

If you owed a significant amount this year, you likely under-withheld your paychecks last year. This can lead to underpayment penalties (and interest) if you don’t pay enough tax throughout the year via withholding or estimated payments.

Plus, it also means stress at tax time from scrambling to find the means to pay a large, unexpected bill.

2. You received a large refund this tax season

A common misconception I hear from my Tacoma clients is that a big refund is free money. But really, a refund is just an interest-free loan you gave to the government all year.

Think about it:If you received a $3,000 refund, that’s $250 per month you could have put in a high-yield savings account or your 401(k), or used to pay down high-interest debt.

And in a high-inflation environment, the dollars you overpaid early in the year have less purchasing power by the time you get them back.

3. Lifestyle, family, or income changes happen

Beyond your year-end results, certain life changes drastically alter your tax bracket or the credits you are eligible for. You should update your W-4 if any of the following occur:

- Marriage or divorce. Your filing status significantly changes your standard deduction and tax brackets.

- Birth or adoption. Adding a dependent makes you eligible for the Child Tax Credit, which reduces your overall tax liability.

- Buying your own Pierce County home. If your itemized deductions (like mortgage interest and property taxes) exceed the standard deduction, you may need to withhold less.

- Starting a second job. Income from multiple jobs is stacked on top of each other, often pushing you into a higher tax bracket than either employer realizes.

- Spouse starting/stopping work. Your household income fluctuates, which impacts your joint filing status.

- Significant side hustle income. If you have a 1099 side gig, you can often increase your W-4 withholding at your 9-to-5 job to cover the taxes on your freelance earnings, avoiding the need for quarterly estimated payments.

We’re aiming for a near-zero balance. This means you neither owe a large sum nor are waiting on a massive refund.

By adjusting your withholding now, early in the second quarter of 2026, you have the maximum number of pay periods remaining to smooth out your payments and keep your money in your own pocket.

How do I calculate my federal tax withholding?

If you’re wondering, “How do I calculate my federal tax withholding?” The good news is (for the most part) there’s an easy answer: Use the IRS Withholding Estimator tool.

The IRS Estimator is the most efficient way to generate a new W-4, because:

- It accounts for the exact date you’re filing, meaning it can calculate catch-up withholding for the remaining months of 2026.

- It’s updated to factor in new OBBBA provisions, like the no tax on tips and overtime rules, and the new car loan interest deduction.

- It produces a pre-filled W-4 that you can hand to HR without revealing your side-hustle income or your spouse’s salary to your boss.

However, there are some situations where you should understand the manual logic of calculating your withholding:

1. You’re racking in the tips and overtime. The OBBBA grants a tax exemption on the first $25,000 of tips and the first $12,500 of overtime. You must track your YTD totals because once you hit those limits, your tax liability snaps back to your normal bracket. A calculator won’t know exactly when you’ll hit that threshold.

2. You experience equity and bonus spikes (RSUs/ISOs). Bonuses and stock vests are usually withheld at a flat 22% supplemental rate. If your total income puts you in a higher bracket, you are effectively underpaying on every share that vests. You need manual math to calculate the extra dollar amount to add to your W-4.

3. You have a side hustle. If you have side gig business income, there is no employer withholding on those profits. You’ll need to manually calculate the tax owed on your business profit and add it to your W-2 withholding.

4. You’re heading toward a credit phase-out. Certain credits begin to disappear (phase out) once you cross specific income levels. If a mid-year bonus pushes you over that edge, you lose the credit and owe more tax. Manual logic helps you see the cliff coming so you can increase your 401(k) contributions to stay below it.

How to calculate withholding

Step 1: Estimate your total annual tax liability

The most common mistake I see taxpayers make here is calculating withholding based on just a single paycheck. Instead, start with the full picture:

1. Estimate your total 2026 earnings from all sources (wages, bonuses, side hustles, dividends).

2. Subtract deductions. Factor in:

- The standard deduction ($16,100 for Single filers and $32,200 for Married Filing Jointly in 2026)

- Above-the-line deductions like HSA contributions, student loan interest, educator expenses, and deductible IRA contributions.

- Schedule 1-A deductions like those for overtime and tips, car loan interest, and the deduction for seniors.

If you itemize, use your projected total (mortgage interest, property taxes, etc.).

3. Use the 2026 tax tables to calculate the tax on your remaining taxable income. For example, if you are Single and your taxable income is $100,000, your tax is not a flat percentage. It’s a laddered calculation through the 10%, 12%, 22%, and 24% brackets.

4. Subtract any credits you are eligible for (e.g., $2,200 per child under the Child Tax Credit).

So, the formula is:

Total Tax Liability = (Taxable Income times Tax Rates) – Tax Credits

Step 2: Account for Year-to-Date (YTD) payments

Once you know your total tax liability, look at your most recent pay stub. Find the total federal income tax already sent to the IRS, and include any estimated tax payments you’ve made for side income.

Step 3: Calculate the withholding gap

This is the step that fixes a big bill or a big refund. Subtract your YTD payments from your total tax liability to find out what you still owe for the year.

If the result is positive: You are on track for a tax bill.

If the result is negative: You are overpaying and on track for a refund.

Step 4: Determine your per-paycheck target

To reach a $0 balance by year-end, divide your remaining liability by the number of pay periods left in 2026.

How do I adjust my W-4 withholding?

Once you’ve done the math, either manually or using the IRS Tax Withholding Estimator, the final step is implementation.

Here’s how to adjust your withholding to ensure your 2026 paychecks reflect your true tax liability.

1. Access your 2026 Form W-4

Most Tacoma employers no longer use paper forms. You will likely log into your company’s HR or payroll portal. Look for a section titled “Tax Withholding,” “Tax Exemptions,” or “Federal W-4.”

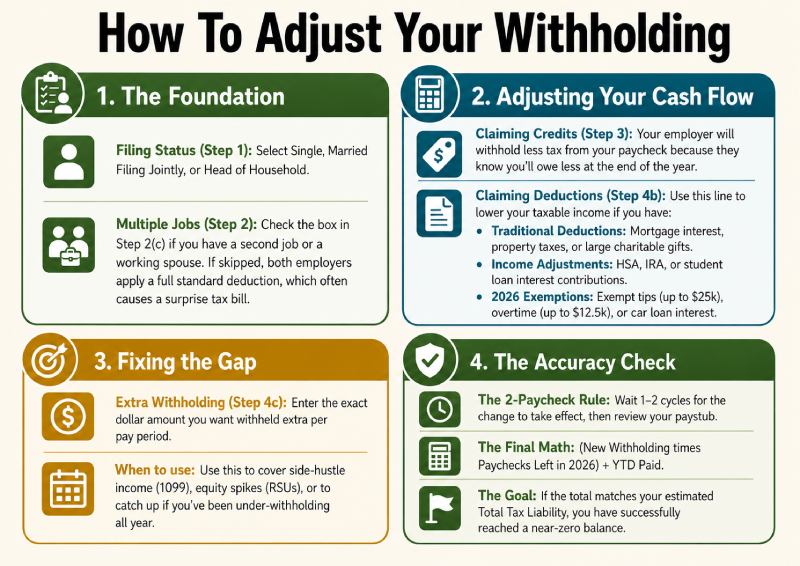

2. Update your filing status and multiple jobs

Ensure your filing status matches what you plan to use on your 2026 return (Single, Married Filing Jointly, or Head of Household).

And if you have a second job or a working spouse, you must check the box in Step 2(c) or use the Multiple Jobs Worksheet. If you skip this, both employers will apply the full standard deduction to your pay, leading to massive under-withholding.

3. Claim your 2026 credits

By filling this out, your employer will withhold less tax from your paycheck because they know you’ll owe less at the end of the year.

4. Account for new deductions

Use this line for all deductions, including traditional mortgage interest, large charitable gifts, and OBBBA deductions like exempt tips, overtime, and the car loan interest deduction.

5. Extra withholding (Step 4(c))

If your manual calculation earlier showed a withholding gap, enter the exact dollar amount you want withheld extra per pay period here.

(Step 4(c) is only for extra tax. If you had a huge refund and want more cash now, you actually increase the amount in Step 4(b) (Deductions) or Step 3 (Credits). This tells the system your taxable income is lower, so it takes out less.)

6. Check your paystub

After you submit your new W-4, wait one to two pay cycles. Then, look at your paystub. Is it higher or lower than you expected?

As another way to check accuracy, multiply your new withholding amount by the number of paychecks left in 2026. Add that to what you’ve already paid (YTD).

If that total matches the total tax liability we calculated earlier, you have successfully broken even.

Final thoughts

Whether you’re tired of giving the government an interest-free loan or you’re still reeling from a surprise bill this April, the point is the same:

Your withholding is the remote control for your cash flow.

Don’t wait until next April to find out if your withholding was correct. Let’s build a proactive strategy that keeps your money with you throughout the year.

calendly.com/legacytaxresolution

FAQs

“When is the best time to adjust my tax withholding?”

The best time to adjust your withholding is after you file your tax return (typically in April or May) or whenever you experience a major life event, such as marriage, having a child, or a significant change in income. Adjusting early in the year allows you to spread any necessary changes across more paychecks.

“Is it better to get a large tax refund or owe a small amount?”

Ideally, you should aim for a break-even point where you owe nothing and receive a minimal refund. A large refund is essentially an interest-free loan you gave to the government. By adjusting your withholding to receive that money in your monthly paycheck instead, you can use it to pay down debt or invest.

“Why did I owe a tax bill even though I had taxes withheld?”

You may owe a tax bill if your withholding didn’t cover your total tax liability. Common reasons include having multiple jobs where each employer applied a full standard deduction, receiving significant 1099 or side-hustle income, or having investment gains (dividends/interest) that weren’t subject to withholding.

“How do I change my tax withholding with my employer?”

To change your withholding, you must submit a new Form W-4 to your employer’s HR or payroll department. Most companies now provide an online employee portal where you can update your filing status, claim dependents, or request an additional dollar amount to be withheld each pay period.

“Can I use my W-4 to cover taxes for my side hustle?”

Yes. If you have freelance or gig income, you can avoid making quarterly estimated tax payments by increasing the withholding at your primary W-2 job. Use Step 4(c) on Form W-4 to enter the extra dollar amount you want withheld from each paycheck to cover your side-hustle taxes.

“How long does it take for a W-4 change to take effect?”

Typically, a withholding adjustment takes effect within one to two pay cycles. However, this depends on your employer’s payroll processing schedule. It is important to check your first few pay stubs after the change to verify that the federal tax withheld matches your new calculations.

“Should I use the IRS Tax Withholding Estimator?”

The IRS Tax Withholding Estimator is a great tool for standard tax situations. However, if you have complex investments, equity compensation like RSUs, or own a business, you should use manual logic or consult a tax professional to ensure you are meeting Safe Harbor requirements and avoiding underpayment penalties.